In an earlier post I began answering the question: “Did the Free Market Cause the Current Crisis?” My short answer is no, but not without qualifications. I argued that three factors led to the housing bubble – the but-for cause of the current recession. Two of the factors are government-related: the Fed and government-created homeownership incentives (I address the latter in this post). Only the third factor, banks’ excessive risk taking, is a direct result of the free market. I will address banks in Part III.

Factor #2: The Government - "Ownership Society"

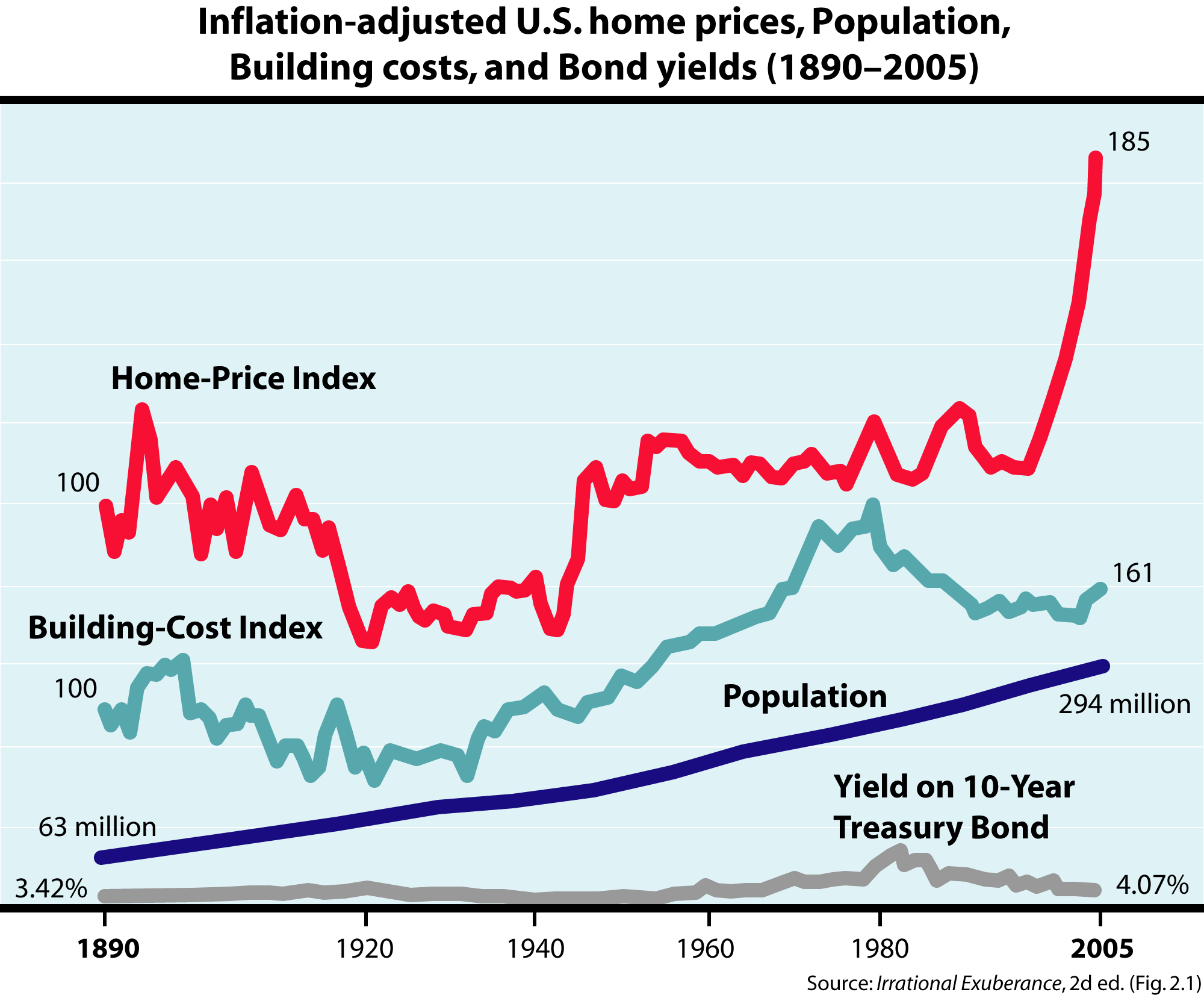

In the late 1990s people began to believe that homes were always safe investments. One reason is that home prices had steadily risen during previous decades, and people simply believed that the increase would continue (behavioral economists call this "status quo" bias). Another reason is that income and population were rising in the 1990s, so more people could afford homes.

As people increasingly viewed homes as safe investments, demand and therefore prices rose. Soon many people were unable to afford 20 percent down payments. People began arguing that low income Americans, especially minorities, were unfairly denied the American dream. Beginning with the Clinton administration, the government began pushing Fannie Mae and Freddie Mac to offer loans to low-income Americans - under the implicit guarantee that the government wouldn't allow these institutions to fail. (This implicit guarantee explains why these institutions could borrow at low rates, despite the fact that they back so many risky loans). The government encouraged lenders to offer loans to people who would be unlikely to afford payments. Unfortunately, the Bush administration continued Clinton's inauspicious policies. President Bush hoped to achieve an “ownership society.” Furthermore, the federal government - and many state governments - began offering strong tax incentives to home buyers.

Still, it's possible to argue that it's a good idea for the government to encourage homeownership because of the positive externality effect: homeowners take better care of their properties than renters do, which increases neighborhood property values. Homeownership may also reduce crime - at least according to Giuliani's "broken window" theory. Nevertheless, as the recent crisis suggests, the government went way too far in its encouragement of homeownership.

The perpetuation of the idea that homes were safe investments and the government's encouragement of homeownership were not independent events. Each fueled the other. These events, along with the Fed's lowering of interest rates and banking deregulation, led to the huge spike in real home prices.

Before claiming that free markets caused the current crisis, however, it’s important to recognize that two of the three culpable events have nothing to do with free markets and everything to with government intervention.

{kind=link}

.png){kind=link}

Dear Committee Members

1 week ago